China’s local government debt may not cause a financial crisis, but it poses a huge fiscal challenge

- China must boost its tax rates and realign tax and expenditure responsibilities so local governments become less dependent on revenue allocations from Beijing and land sales to finance their expenditure

This phenomenon is an outgrowth of China’s skewed fiscal structure. In China, provincial and municipal governments lack broad taxation powers; those are jealously guarded by Beijing.

Yet, the central government relies on its local counterparts to fund and provide the bulk of infrastructure and social services. So, provinces are chronically short of revenue but burdened with spending obligations.

For many local governments, establishing LGFVs allows them to spend beyond their restricted means. That debt is better categorised as government liabilities than corporate debt.

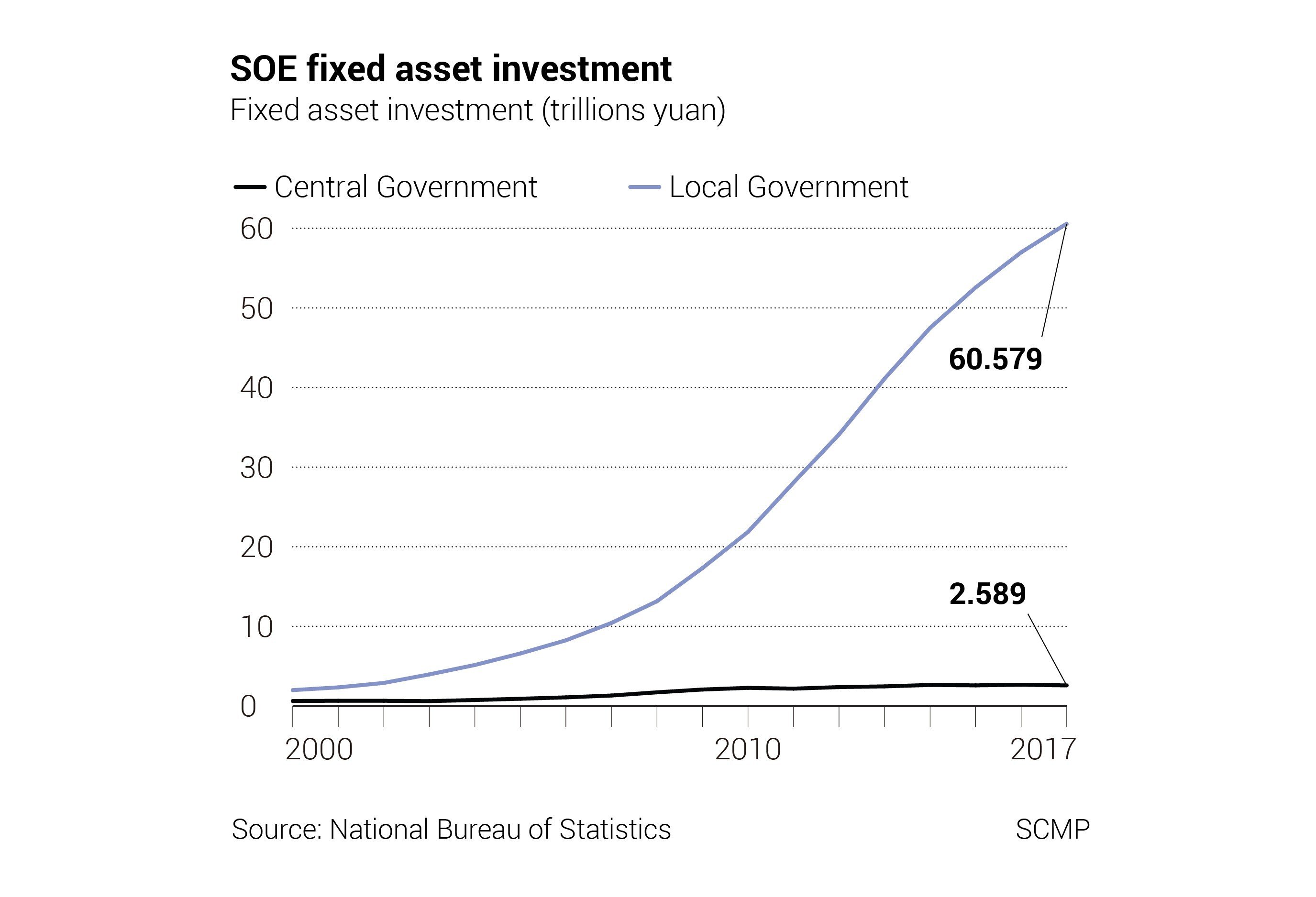

Local governments have poured the funds raised by the floating of bonds via LGFVs into infrastructure projects. In 2000, the levels of fixed asset investment undertaken by SOEs that were locally and centrally run were similar.

By 2017, enterprises controlled by local governments were doing over 20 times as much investment as those directed from Beijing, reflective of consistent budget shortfalls.

As long as land assets were appreciating more rapidly than interest rates were climbing, local governments could keep rolling over their debt.

At some point, defaults of LGFVs and other SOEs might be a legitimate reason for worry, perhaps as harbingers of a broader financial crisis. But that is unlikely.

S&P Global Ratings downgraded the creditworthiness of some, but not all, LGFVs last April when pandemic-related lockdowns were at their peak in China. The rating agency noted that much of the LGFV debt is effectively guaranteed by provincial governments.

So, even when changing the outlook of several such bonds to “negative”, S&P noted that the likelihood of extraordinary government support had increased to “almost certain” or “very high”.

The People’s Bank of China has kept interest rates at historic lows, partly in response to the pandemic. This has made it easier for SOEs to roll over their debt, reducing the chances of widespread collapse.

Beijing has expressed a greater willingness to let some SOEs, including LGFVs, default on their debts. But that hardly translates into carte blanche to abandon all (implicitly) government-backed borrowing.

Even in an unlikely worst-case scenario, if all LGFVs had to default on their outstanding debt simultaneously, a purchase of those toxic assets worth 9 trillion yuan would increase the government debt-to-GDP ratio by 12 percentage points.

This calculation doesn’t consider the second-order ramifications or the liquidity effects it might have on interbank lending. But with quick PBOC intervention, a worst-case fallout could be contained.

The other is to realign tax and expenditure responsibilities so local governments become less dependent on revenue allocations from Beijing and land sales to finance their expenditure.

Yukon Huang is a senior fellow at the Carnegie Endowment for International Peace. He is author of Cracking the China Conundrum: Why Conventional Economic Wisdom Is Wrong. Joshua Levy is a junior fellow at the Carnegie Endowment for International Peace